Summer 2024 Newsletter

Volume 11, Issue 1

The State of Carton End Markets in North America, 2024 – Q&A with Jason Pelz, Vice President of Recycling for the Carton Council of North America

Jason Pelz, Vice President of Recycling for the Carton Council of North America.

How would you describe the current state of end markets for cartons in North America?

The markets for cartons in North America are as stable as they have been in a very long time. MRFs and other operators who have loads of cartons to move are able to move them, whether it’s to a location in North America or overseas. While there are certainly opportunities for improvement, in general carton recycling facilities are running well, setting the industry up for growth.

Are there any new developments that you would like to share with us?

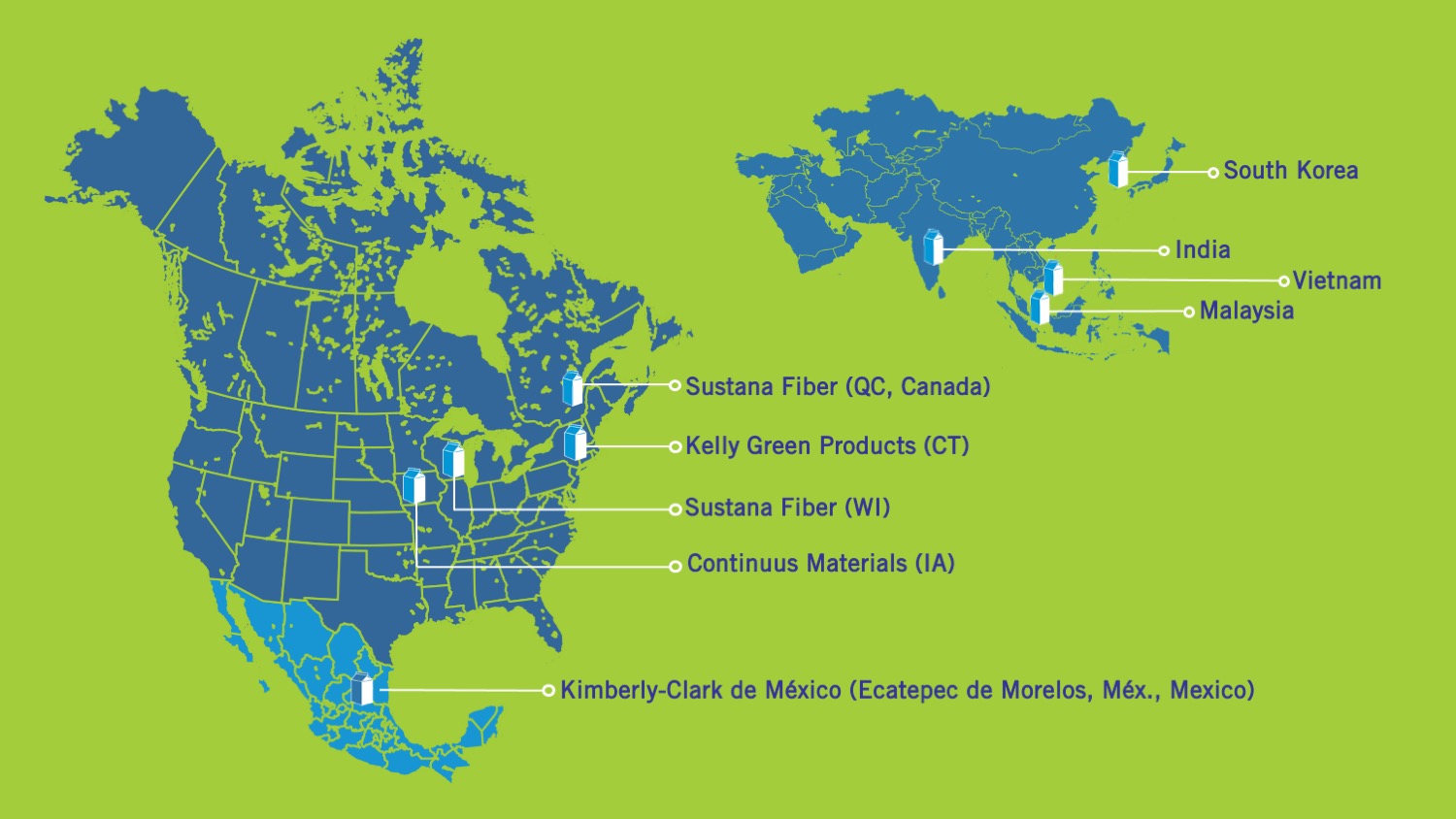

There are a few developments to note. For instance, Sustana continues to increase their focus on cartons and on cartons’ importance as a feedstock for their products. Likewise, the Continuus Materials facility in Des Moines, Iowa (see article on a recent visit to the facility in this edition of our newsletter) has recently added new equipment and capacity, which we expect to see the benefit of in a couple of months. And finally, Essity’s paper mill in Alabama has recently started taking used food and beverage cartons, bringing the total number of carton end markets in North America to six.

Recyclers of used carton bales (grade PSI-52) in North America and elsewhere as of May 2024.

How have recent market trends impacted the development of end markets?

The two primary applications where used cartons are getting used are either in building products, where there seems to be good demand, or as a replacement for office paper and other printing and writing grades, where the generation of those materials continues to decline in availability.

How has pricing impacted the development of potential end markets? Do you see this changing any time soon?

The CCC recently compiled the ten-year market value of cartons in Ontario and Quebec, as reported by the Continuous Improvement Fund’s Price Sheet and RECYC-QUÉBEC’s Recycled Materials Price Index, respectively. Over this time period, commodity pricing for used food and beverage cartons in both provinces has been superior or comparable to pricing for mixed paper, with the notable exceptions of 2021 and 2022. The average price over this ten-year period was $59 for cartons and $39 for mixed paper in Ontario and $77 and $52 in Quebec, a difference of 51% and 48%, respectively.

I think it’s fair to say that we expect carton pricing to continue trending in the right direction as demand grows.

With the recent discontinuation of Ontario’s Price Sheet, readers interested in keeping informed on carton pricing can consult the Davis Index for recovered paper, a subscription-based service which provides domestic and export pricing for a variety of grades, including cartons (PSI-52).

Are there any emerging technologies or innovations affecting the carton recycling market?

I think even more than new technology, we’re seeing more creative approaches among the end users and the recycling markets to use post-consumer food and beverage cartons. The reality is that certain recovered materials don’t or won’t exist anymore and companies are adapting and finding ways to find substitutions to those grades. It takes time and ingenuity, but it happens—and sometimes it’s not even about new technology so much as it is about new ways of thinking and working with the equipment recyclers already have.

The above is specific to post-consumer cartons when being consumed as a specific carton grade or even as part of a polycoat grade. When we talk about cartons and mixed paper, there have been some developments with new pulping technology that is making it easier for mills to accept and use cartons as part of mixed paper. That can be a game changer. The NORPAC mill in Longview, Washington State is an excellent example of this. The technology used in the pulper installed in 2022 allows them to take cartons in mixed paper bales and extract the fibre to be used in their paper products.

What are the challenges or barriers facing the expansion of end markets in North America?

In order to be able to use cartons, you have to be able to handle polyal and you have to be able to handle wet strength. And that’s the challenge because you either need the equipment that can do that, be willing to try to get your existing equipment to do it or be willing to upgrade your equipment. Many mills are realizing that their primary fibre, office paper, is eventually going to go away. If they can’t figure out how to run alternative fibres, they’re going to be in some trouble. It’s not necessarily an easy transition but, in some instances, will be a necessary one. But it can be hard to turn a ship. I hope mills keep in mind that Carton Council is here to help if there is interest in finding ways to incorporate cartons into their mix.

What strategies are being employed to encourage the development of new end markets?

The biggest strategy I see is information sharing. It’s meeting with the right people to help others understand the opportunities in the market and the value of cartons. It’s knowing who might benefit from the inclusion of cartons as an input for what they make. And then, once the door is open to the discussion, it’s about strategies that can help the vision come to life—including things like grant funding opportunities, technical support, help regarding best practices, etc.

It is true, though, that as an industry we need to constantly be on the lookout for innovative ways to apply creative thinking and technology and to proactively support these efforts. For example, CCC recently partnered with a research centre to test the suitability of cartons in moulded fibre applications. The results of these trials are promising (more on this soon) and we plan on sharing them broadly with industry stakeholders in order to generate interest in new carton recycling applications.

What is your 3–5-year prediction for carton end markets in North America? Around the world?

I believe the industry is set up for expansion. This is true for two reasons:

- The future for building products made from recycled cartons is bright. I would expect more of these facilities to pop up within Canada and the U.S. and around the world. Overall, this type of manufacturing doesn’t require a huge footprint, nor does it require the use of water or chemicals, so it can be relatively easy to set up, which is promising. In fact, readers can look forward to an exciting announcement coming from the West Coast soon.

- From the paper mill side of things, it’s fair to expect more interest in cartons because of the declining availability of other feedstocks, like office paper, and the replacement potential that cartons present.

I think it’s also important to remember that we need to be patient. There is often an assumption that these kinds of changes should happen quickly and that’s just not the case. It takes a lot of trial and error, and a lot of long negotiations. That said, we’re beginning to see the benefits of being persistent and working on these kinds of initiatives. Sometimes there are setbacks, but we regroup and move on. It’s not always a linear progression, but it is progress, nonetheless.

Contents

- The State of Carton End Markets in North America, 2024 – Q&A with Jason Pelz, Vice President of Recycling for the Carton Council of North America

- CCC Visits Three North American Carton End Markets With Recycling Partners

- Provincial Studies, National Survey Help Illustrate Recycling Behaviour and Perceptions Across the Country

- Municipality of Dysart et al in Ontario Conducts Awareness Project With CCC Funding

- Carton Council of Canada Launches 2024 Community Education Award in Alberta, Saskatchewan and Manitoba